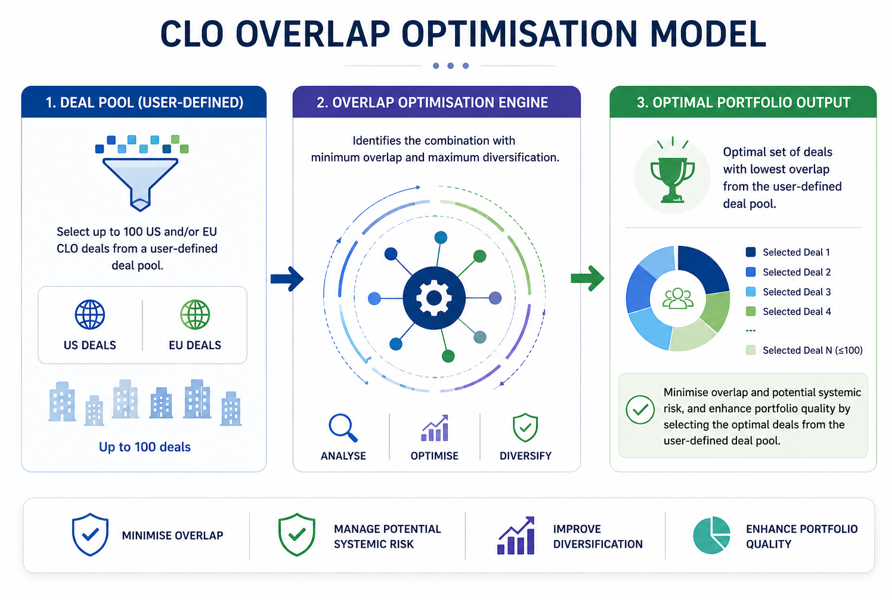

AAA/AA investors are always thinking about systemic risks, and one way to reduce this risk is to minimise overlap exposure within their portfolios. The beauty of this model is that users can choose from a pool of CLO deals managed by managers they favour and optimise the portfolio for the lowest possible overlap risk based on the target number of positions they are looking to hold. Please find the download link below for the overlap optimisation model, which allows users to select from a pool of US BSL CLO deals to be added to an existing portfolio, with the model identifying the optimal outcome from an overlap perspective.

For existing premium subscribers, please log in here.

If you'd like to find out more about premium subscription, please submit the form below: